Credit Union Loan Rates: Compare & Calculate Your possible option

Did you know 1 in 3 Americans have errors on their credit reports? This guide reveals practical 2026 strategies to understand and improve your credit profile fast, legally, and without costly services.

Credit Union Loan Rates: The Overlooked Advantage

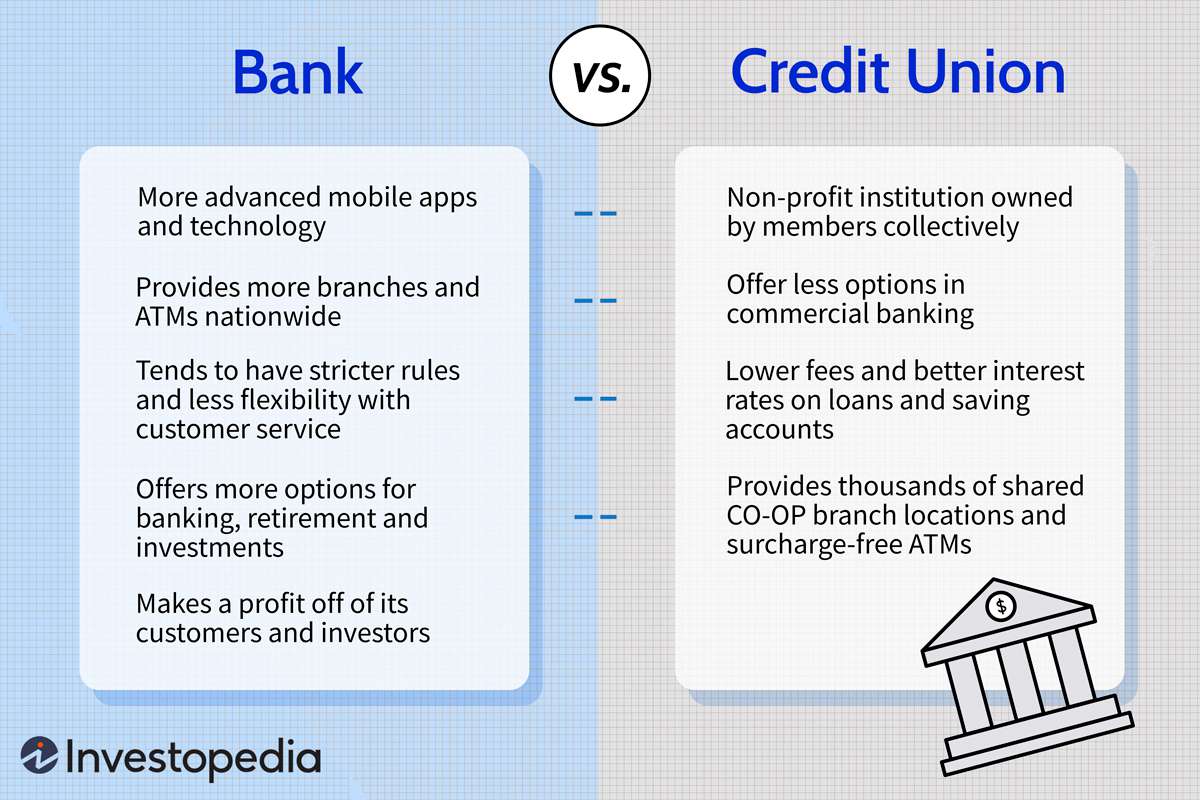

In the complex landscape of borrowing, where banks dominate the advertising space, credit unions operate with a distinct, member-focused philosophy that translates into tangible financial benefits – most notably, their loan rates. While often overshadowed by larger institutions, credit unions consistently offer a compelling alternative precisely because their structure prioritizes member value over shareholder profit. Understanding why their rates differ is key to making an informed borrowing decision.

What Are Credit Union Loan Rates?

Simply put, credit union loan rates represent the cost of borrowing money from a member-owned financial cooperative. Unlike banks driven by maximizing returns for external investors, credit unions return their profits to members, primarily through more favorable loan rates and lower fees.

Definition and Core Importance

Credit union loan rates are the annual percentage rates (APR) charged on various loan products – auto loans, personal loans, mortgages, and credit cards. Their importance cannot be overstated:

- Direct Cost Savings: Even a fractionally lower rate can save borrowers hundreds or thousands of dollars over the life of a loan. On average, credit union loan rates are 1-2 percentage points lower than comparable bank rates in 2026.

- Accessibility: Lower rates make borrowing more affordable, increasing access to essential financing like cars or home improvements for members who might be priced out by traditional bank offerings.

- Member-Centric Value: Competitive rates are a fundamental expression of the credit union “people helping people” philosophy, directly fulfilling their mandate to serve members’ best interests.

Crucially, loan rates can vary significantly between credit unions. Factors influencing this variation include:

- The credit union’s operational costs and efficiency.

- Local economic conditions and competitive landscape.

- The specific field of membership (e.g., employer-based, community-based).

- The loan type, term, and the individual borrower’s creditworthiness.

| Loan Type (2026 Avg.) | Credit Union Avg. Rate | Bank Avg. Rate | Potential Savings (60-mo $25k loan) |

|---|---|---|---|

| New Auto Loan | 5.25% | 6.75% | ~$1,100 |

| 3-Year Personal | 8.50% | 10.99% | ~$400 |

| 30-Yr Fixed Mtge | 6.10% | 6.65% | ~$35,000+ (over loan life) |

Why Choose a Credit Union for Your Loan?

The decision often boils down to value alignment. Credit unions offer a fundamentally different financial relationship, one centered on the member-borrower.

Tangible Advantages Over Traditional Banks

Choosing a credit union for a loan isn’t just about potentially lower numbers on paper; it’s about accessing a more equitable and supportive borrowing experience:

- Lower Rates & Fees: As their not-for-profit structure dictates, credit unions consistently offer lower APRs on loans and charge fewer and lower fees (e.g., application fees, origination fees, prepayment penalties). The savings highlighted in the table above are a direct result of this model.

- Superior Customer Service: Credit unions are renowned for personalized service. Loan officers often have more flexibility and time to understand individual circumstances, potentially leading to more tailored solutions or consideration for borderline credit situations compared to the rigid algorithms often employed by large banks.

- Member Ownership & Community Focus: When you borrow from a credit union, you’re not just a customer; you’re a member-owner with a vote. This fosters a sense of accountability to the membership. Profits are reinvested into offering better rates, lower fees, and improved services for the members, not distributed to distant shareholders. This often translates into a strong focus on supporting the local community’s financial health.

- Transparency & Trust: The member-owned model inherently promotes greater transparency in lending practices. Credit unions have a vested interest in ensuring members understand their loan terms and succeed financially, building long-term trust rather than maximizing short-term profit on a single transaction.

The difference is structural. Banks answer to Wall Street; credit unions answer to Main Street. This foundational distinction is why, when searching for the most advantageous loan terms coupled with respectful service in 2026, exploring options from reputable credit unions isn’t just an alternative – it’s often the financially smarter choice. Finding the best fit for your specific loan need requires comparison, and resources like those offered by fixcreditscenter.com can streamline the process of identifying credit unions offering rates and terms that genuinely work for you.

Current Trends in Credit Union Loan Rates

The landscape of credit union loan rates in 2026 is shaped by broader economic currents, primarily the movement of the benchmark interest rate set by central banks. Understanding these trends provides crucial context for borrowers seeking the best terms.

The landscape of credit union loan rates in 2026 is shaped by broader economic currents, primarily the movement of the benchmark interest rate set by central banks. Understanding these trends provides crucial context for borrowers seeking the best terms.

Prime Rate and Its Impact

The prime rate serves as the fundamental anchor for variable-rate lending across the financial system, including credit unions. It directly influences the cost of borrowing for consumers.

Understanding Prime Rate

- The Servus Prime Rate, a widely recognized benchmark, stands at 4.95% as of March 15, 2026. This rate reflects the cost at which major financial institutions lend to their most creditworthy customers.

- Credit unions typically set their variable-rate loan products (like lines of credit, adjustable-rate mortgages (ARMs), and some variable personal/auto loans) as a spread above the prime rate.

- For example, a credit union might offer a home equity line of credit (HELOC) at “Prime + 0.50%”, resulting in a rate of 5.45% based on the current Servus Prime.

- Impact: When the central bank adjusts its target rate (influencing prime), rates on these variable credit union loans move correspondingly. A rising prime rate increases borrowing costs for holders of variable-rate loans; a falling prime rate decreases them. Fixed-rate loans, however, are locked in at origination and remain unaffected by subsequent prime rate changes during their term.

Historical Trends and Future Projections

Examining the trajectory of credit union loan rates reveals patterns and offers insights into potential future movements, though projections remain inherently uncertain.

Loan Rate Trends Over the Last Decade

- Post-Pandemic Volatility: The period following the global pandemic saw historically low rates, with credit union offerings hitting unprecedented lows, particularly for mortgages and auto loans. This was driven by aggressive central bank easing to stimulate economies.

- The Inflation Surge & Response (2022-2026): As inflation surged globally, central banks embarked on rapid and significant rate hikes. Credit union loan rates followed suit, rising sharply across all major product categories (auto, personal, mortgage) to levels not seen in over 15 years. The pace of increase was dramatic compared to the gradual declines of the preceding decade.

- Recent Stabilization (Late 2026 – Early 2026): Following peak inflation, central banks have held rates steady. Credit union loan rates have largely plateaued in early 2026, reflecting this pause. However, they remain significantly higher than the lows of 2020-2021.

- Consistent Advantage: Crucially, throughout this volatile decade, credit unions maintained their relative rate advantage over traditional banks, typically offering rates 1-2 percentage points lower on comparable loans, as evidenced in historical data and the 2026 comparison table provided earlier. Their not-for-profit structure provided a buffer, allowing them to pass on savings more effectively even during rising rate environments.

Future Outlook for 2026 and Beyond:

- Near-Term (Next 1-2 Quarters): Consensus among economists suggests the Servus Prime Rate (and thus variable credit union loan rates) is likely to remain relatively stable through mid-2026. Central banks are closely monitoring inflation data and are expected to maintain current policy unless significant deviations occur.

- Potential for Modest Declines (Late 2026/Early 2026): Many forecasts point towards the possibility of gradual rate cuts starting in late 2026 or early 2026, assuming inflation continues to trend towards target levels. This would lead to corresponding decreases in credit union variable loan rates and potentially ease pressure on new fixed-rate loan pricing.

- Uncertainty Factors: Geopolitical events, unexpected economic data (e.g., job reports, inflation prints), and shifts in central bank communication can rapidly alter the projected path. Borrowers should remain aware of this inherent uncertainty.

- Credit Union Resilience: Regardless of the direction, the structural advantage of credit unions – their member-focused model translating into lower operational costs and a mandate to return value – positions them to continue offering consistently competitive rates compared to for-profit banks. Monitoring rate trends and comparing offers remains essential, and tools available through resources like fixcreditscenter.com can simplify identifying the most advantageous credit union loan options tailored to your needs in this evolving rate climate.

Types of Loans and Their Rates

Building upon the broader economic trends shaping credit union lending, the specific rates offered on different loan products reveal the tangible advantages for members. Credit unions leverage their not-for-profit structure to translate stability, like the current plateau in the Servus Prime Rate at 4.95%, into competitive pricing across diverse borrowing needs. This section details prevalent loan categories and their current rate landscape for 2026.

Building upon the broader economic trends shaping credit union lending, the specific rates offered on different loan products reveal the tangible advantages for members. Credit unions leverage their not-for-profit structure to translate stability, like the current plateau in the Servus Prime Rate at 4.95%, into competitive pricing across diverse borrowing needs. This section details prevalent loan categories and their current rate landscape for 2026.

Personal Loans

Personal loans from credit unions provide flexible financing for expenses ranging from debt consolidation to home improvements, typically offering significantly lower rates than credit cards or traditional bank unsecured loans. Their structure is usually straightforward: a fixed amount borrowed, repaid over a set term with fixed monthly payments.

Current Rates and Examples

- Competitive Entry Points: Leading credit unions offer attractive starting rates. For instance, Servus Credit Union lists its personal term loans starting at 8.50% as of early 2026. This represents a substantial saving compared to average bank offerings for similar unsecured credit.

- Specialized Value: Some credit unions provide unique products catering to specific values. Christian Credit Union, for example, offers a “Personal Charity Loan” at a notably low rate of 5.50%. This loan allows borrowers to direct a portion of the interest paid back to a charity of their choice, demonstrating the member-centric approach while delivering exceptional value.

- Rate Determinants: While starting rates are appealing, the final Annual Percentage Rate (APR) offered to an individual member is heavily influenced by:

- Creditworthiness: Stronger credit scores typically secure the best advertised rates.

- Loan Amount & Term: Larger loans or shorter terms might sometimes qualify for marginally better rates.

- Membership & Relationship: Existing members, especially those with multiple products (like checking/savings accounts), may receive preferential pricing.

| Credit Union | Personal Loan Product | Starting Rate (2026) | Key Feature |

|---|---|---|---|

| Servus Credit Union | Standard Personal Term Loan | 8.50% | Flexible use, fixed payments |

| Christian CU | Personal Charity Loan | 5.50% | Portion of interest supports charity |

Mortgage Options

For most individuals, a mortgage represents the largest financial commitment. Credit unions are major players in this market, offering both fixed-rate stability and variable-rate potential savings, consistently undercutting big bank pricing.

Fixed vs. Variable Rate Mortgages

The fundamental choice for borrowers hinges on risk tolerance and outlook on future interest rates:

- Fixed-Rate Mortgages: Offer certainty. The interest rate is locked in for the entire term (commonly 1-5 years). Payments remain constant, unaffected by fluctuations in the prime rate. This is ideal for budgeting certainty, especially if rates are expected to rise. Example: A competitive 5-year fixed-rate mortgage might be offered around 4.39% by select credit unions in early 2026.

- Variable-Rate Mortgages (VRMs): The interest rate fluctuates with changes in the lender’s prime rate (e.g., Servus Prime + a fixed spread). Payments can increase or decrease over the term. VRMs often start with a lower rate than fixed mortgages, offering potential savings if prime rates fall or remain stable, but carry the risk of higher payments if rates rise. Example: A VRM might be priced at “Prime – 0.60%” (currently 4.95% – 0.60% = 4.35%).

Current Mortgage Rates from Various Credit Unions

Credit union mortgage rates are highly competitive nationally. While specific rates vary daily and depend heavily on the borrower’s profile (down payment, credit score, property type), the landscape in early 2026 shows:

- Fixed Rates: Generally ranging from the low 4% range for shorter terms (1-2 years) to the mid-to-high 4% range for popular 5-year terms. The 5-year fixed rate often serves as a key benchmark.

- Variable Rates: Typically priced as a discount below the prime rate (e.g., Prime – 0.40% to Prime – 0.80%), translating to rates often below 4.50% based on the current Servus Prime of 4.95%. The discount offered can be a major differentiator.

- The Credit Union Edge: Historical data and ongoing comparisons confirm that credit unions frequently offer mortgage rates 0.50% to 1.50% lower than those advertised by major chartered banks for equivalent products and borrower profiles. This advantage stems directly from their lower operating costs and member-focused mandate.

Choosing between fixed and variable requires careful consideration of one’s financial stability and interest rate outlook. While fixed offers peace of mind, variable can provide significant initial savings, particularly relevant in the current climate of potential rate stability or future declines projected for late 2026. Regardless of the choice, securing the best possible terms demands comparison shopping. Resources like fixcreditscenter.com simplify this process, allowing potential borrowers to efficiently compare real-time credit union mortgage rates and find the optimal fit for their home financing needs in 2026.

Impact of Loan Rates on Financial Planning

The concrete numbers defining credit union loan rates in 2026—whether it’s a personal loan starting at 5.50% or a 5-year fixed mortgage hovering around 4.39%—aren’t just isolated figures. They form the bedrock of effective financial planning, influencing monthly cash flow and long-term wealth accumulation in profound ways. Securing a favorable rate fundamentally reshapes what’s possible with your money.

The concrete numbers defining credit union loan rates in 2026—whether it’s a personal loan starting at 5.50% or a 5-year fixed mortgage hovering around 4.39%—aren’t just isolated figures. They form the bedrock of effective financial planning, influencing monthly cash flow and long-term wealth accumulation in profound ways. Securing a favorable rate fundamentally reshapes what’s possible with your money.

Budgeting for Loans

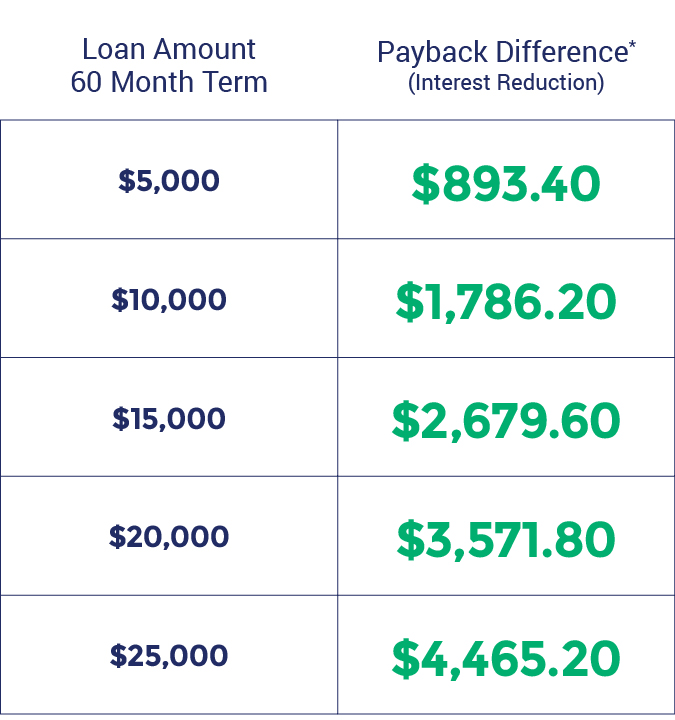

Accurately forecasting the impact of a loan on your monthly budget is non-negotiable. The difference between a 5.50% and an 8.50% personal loan, as seen in credit union offerings, translates into hundreds, sometimes thousands, of dollars saved over the loan term.

Calculating Loan Affordability

Understanding your potential monthly payment before applying is crucial. This is where specialized tools become indispensable:

- Online Loan Calculators: Reputable credit unions and independent financial sites provide free calculators. Input the loan amount, the interest rate (using current benchmarks like the 8.50% starting point for standard personal loans or 4.39% for a 5-year fixed mortgage), and the term. The calculator instantly outputs the estimated monthly principal and interest payment.

- Key Budgeting Factors: Beyond the calculator result, integrate these into your budget forecast:

- Total Interest Cost: A lower rate drastically reduces the total amount paid over the life of the loan. That 5.50% charity loan from Christian CU, for instance, builds significant savings versus higher-rate alternatives.

- Existing Debt Obligations: Factor in all current loan/credit card payments. Debt-to-income ratio (DTI) is a critical metric lenders assess, and staying below 36% is generally advisable.

- Rate Determinants Impact: Remember that your final rate hinges on creditworthiness and relationship status. Budgeting scenarios should include best-case (lowest advertised rate) and worst-case (higher rate) possibilities based on your credit profile. Securing that preferential rate through strong credit or membership benefits directly increases disposable income.

- Emergency Buffer: Never allocate every spare dollar to loan repayment. Maintain a cushion for unexpected expenses to avoid jeopardizing your payment schedule.

Long-term Investment Perspective

Loan rates act as a powerful counterforce to investment returns. A high-interest loan erodes wealth-building capacity, while a low rate preserves capital for growth. Integrating loan decisions into your broader investment strategy is essential for true financial health.

Integrating Loan Payments into Investment Strategy

Viewing loan payments solely as an expense overlooks their strategic role. Consider these dynamics:

- The Opportunity Cost of Interest: Every dollar paid in interest on a loan is a dollar not compounding in your retirement account or investment portfolio. The 0.50% to 1.50% average rate advantage credit unions hold over big banks for mortgages, as noted earlier, translates directly into preserved capital. Over a 25-year mortgage term, this differential can equate to tens of thousands of dollars retained for investment.

- Impact on Compound Growth: High-interest debt, especially from credit cards or costly personal loans, cripples the magic of compound interest on savings. Prioritizing debt repayment at lower credit union rates (like consolidating high-interest debt into an 8.50% personal loan) often yields a higher effective “return” than conservative investments by eliminating promised high-interest expenses.

- Retirement Planning Synergy: Loan choices made today ripple through retirement. A lower mortgage rate (e.g., 4.39% fixed vs. a bank’s 5.39%) means lower mandatory monthly outlays during retirement years. Conversely, carrying high-interest debt into retirement drastically increases the required nest egg. Proactively securing the best possible credit union loan rates in 2026 frees up cash flow that can be systematically invested earlier, leveraging time for growth. Evaluating loan options requires the same diligence as choosing investments; platforms like fixcreditscenter.com offer the necessary tools to compare real-time credit union rates, ensuring your borrowing strategy actively supports your long-term investment and retirement objectives.

Finding the Best Credit Union Loan Rates

Navigating the landscape of credit union loan rates in 2026 requires more than just a cursory glance at advertised numbers. While the foundational rates—like personal loans starting at 5.50% or 5-year fixed mortgages near 4.39%—provide a benchmark, the actual rate you secure is profoundly personal. It hinges on where you look and how you prepare. Finding the optimal rate isn’t merely about saving money next month; it’s about unlocking the long-term financial flexibility discussed earlier, freeing capital for investment or accelerating debt freedom.

Navigating the landscape of credit union loan rates in 2026 requires more than just a cursory glance at advertised numbers. While the foundational rates—like personal loans starting at 5.50% or 5-year fixed mortgages near 4.39%—provide a benchmark, the actual rate you secure is profoundly personal. It hinges on where you look and how you prepare. Finding the optimal rate isn’t merely about saving money next month; it’s about unlocking the long-term financial flexibility discussed earlier, freeing capital for investment or accelerating debt freedom.

Comparing Different Credit Unions

Not all credit unions are created equal, especially in 2026. While they consistently offer member-focused value, the specifics of their loan products—rates, terms, fees, and accessibility—can vary significantly. Treating them as a monolithic group means potentially leaving savings on the table.

Key Factors to Consider

When evaluating credit unions for a loan, look beyond the headline interest rate:

- Interest Rates, Terms, and Fees: Scrutinize the fine print. A slightly lower rate might be offset by hefty origination fees, prepayment penalties, or mandatory insurance products. Compare the Annual Percentage Rate (APR), which incorporates most fees, for a true cost comparison. For instance, a charity personal loan from Christian CU at 5.50% APR is vastly different from another credit union’s standard personal loan advertised at 8.50% plus significant fees pushing the effective APR higher.

- Accessibility & Service Model: Consider your banking preferences. Does the credit union offer robust online and mobile banking for seamless loan management and payments? Are local branches convenient if in-person service is important? In 2026, digital-first credit unions might offer highly competitive rates but lack physical branches, while larger community-based ones blend local presence with strong digital tools. Ensure their service model aligns with your needs.

Table: Typical 2026 Credit Union Loan Rate Ranges (Illustrative)

| Loan Type | Typical Starting APR Range | Key Notes |

|---|---|---|

| Personal Loan | 5.50% – 12.99%+ | Deeply tiered based on credit score & membership |

| 5-Yr Fixed Mtge | 4.39% – 5.50%+ | Relationship discounts common |

| Auto Loan (New) | 4.99% – 7.50%+ | Often beats bank & captive financing |

| Credit Card | 11.99% – 17.99%+ | Lower than national average; rewards vary |

Tips for Securing the Best Rates

Securing the most favorable credit union loan rate in 2026 isn’t passive; it’s an active process requiring preparation and strategy. Your creditworthiness and approach directly influence the rate offered, impacting the long-term investment math discussed previously.

Improving Your Credit Score

Your credit score remains the single most powerful lever you control in the loan rate equation. A higher score signals lower risk, translating directly into lower interest rates offered.

- Steps Before Applying: Obtain your official credit reports (free annually) and meticulously review them for errors. Dispute any inaccuracies immediately. Focus on paying down revolving debt (especially credit cards) to lower your credit utilization ratio, a major scoring factor. Ensure all bills are paid on time, every time. Even a modest score increase—say, moving from “Good” (670-739) to “Very Good” (740-799)—can shave significant tenths of a percentage point off your loan APR.

- The Pre-Application Window: Avoid applying for new credit (credit cards, other loans) in the 3-6 months before your target loan application. Each application typically triggers a hard inquiry, which can temporarily ding your score. Consolidate your credit report review and improvement efforts well in advance.

Importance of Shopping Around

Rates and terms vary between credit unions, even for applicants with identical credit profiles. Casting a wide net is crucial.

- Leverage Pre-Qualification: Many credit unions offer rate pre-qualification using a soft credit check (which doesn’t affect your score). This provides personalized rate estimates without commitment. Use this tool extensively.

- The Rate Shopping Window: Credit scoring models generally treat multiple inquiries for the same type of loan (e.g., mortgage, auto loan) within a short period (typically 14-45 days) as a single inquiry for scoring purposes. This encourages comparison shopping. Gather pre-qualifications from 3-5 credit unions within this focused window.

- Negotiate & Leverage Relationships: Don’t assume the first offer is final. If you have a strong existing relationship (checking/savings accounts, other products) with a credit union, highlight it. Mention competing offers you’ve received – loyalty and competition can sometimes unlock an even better rate tier. Remember, the 0.50% to 1.50% average advantage credit unions hold over banks represents potential savings worth fighting for; actively comparing real-time offers through platforms like fixcreditscenter.com ensures you capture that advantage fully for your specific loan need.

5 things to know About Balance Transfer Credit Cards for rebuilding credit

How Long Does a Repo Stay on Your Credit Report

7 Key Things About Your Credit Card for Fair Credit Journey

5 Free Ways to Monitor Your FICO® Score with myFICO

Unlock Your Financial Future: Free Credit Score Repair Certification Explained

Key Takeaways for Credit Repair Success

By following these steps – checking reports regularly, disputing errors, and managing payments – you’re now equipped to rebuild your credit. Remember, improvement takes time but starts today.

Ready to take control? Visit https://fixcreditscenter.com now for personalized tools. Share your progress below or tag a friend who needs this!

Disclaimer

This article is for educational purposes only and does not constitute legal, financial, or credit repair advice. FixCreditsCenter.com does not promise credit score increases, credit approval, or removal of accurate negative information. Results vary based on individual credit history.