7 Power Moves to Fix Credit Score After Late Payments

Did you know a single late payment can slash meaningful score movement off your credit score? Learn how late payments linger for 7 years and discover 2026’s fastest repair strategies.

Why Late Payments Haunt Your Credit

Late payments are more than just a temporary setback; they embed themselves into your credit history, creating lasting ripples that impact your financial opportunities. Understanding how and why they damage your score is crucial for navigating the path to recovery.

How One Late Payment Drains Your Score

The impact of a single late payment can feel disproportionately important, and that’s largely due to the structure of the FICO scoring model, the system used by most lenders in 2026. Your payment history isn’t just important; it’s the single most influential factor in your credit score.

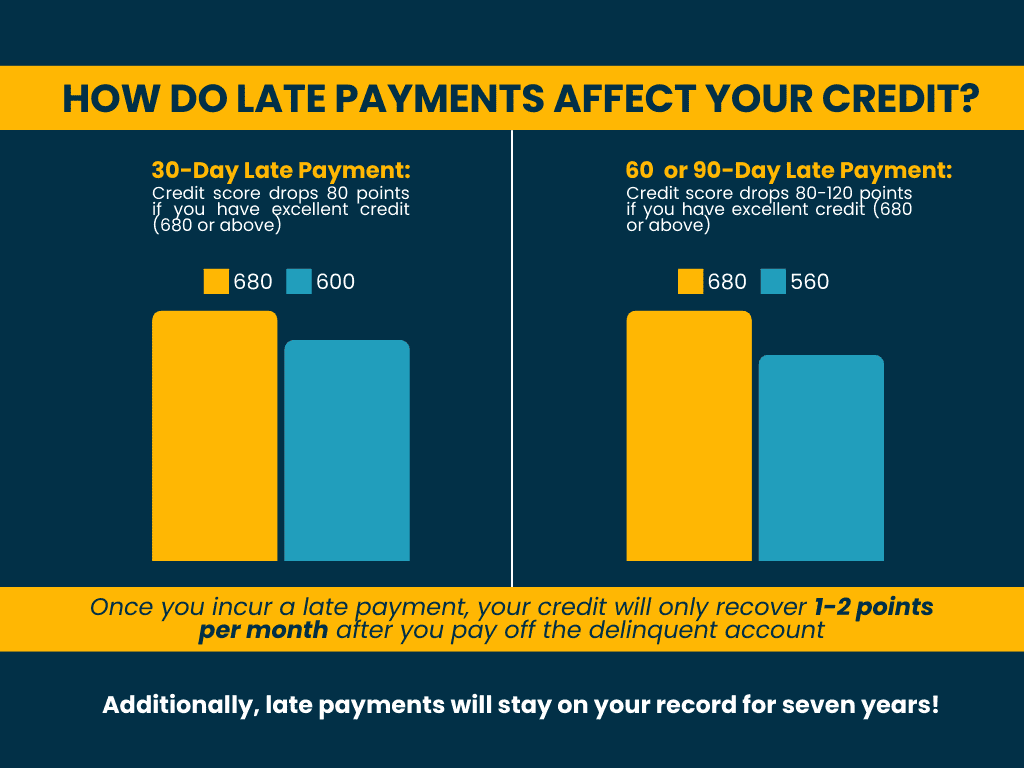

- FICO Scoring Breakdown Reveals Payment History Weight: This critical component accounts for a substantial 35% of your overall FICO score. Consistently paying on time is the bedrock of a strong credit profile. When a payment slips past its due date, even by just a day, lenders typically report it to the credit bureaus once it reaches the 30-day late mark. This single event signals potential risk to future lenders.

- The Initial Shock: The effect of that first reported 30-day late payment is often immediate and significant. While individual impacts vary based on your overall credit history and score starting point, it’s common to see a drop of 50 to large score jump or more. Someone with a previously pristine 780 score could easily find themselves in the high 600s or low 700s after just one late payment hits their report. This sudden drop can push you out of the best interest rate tiers for loans and credit cards.

The Domino Effect of Multiple Delinquencies

While one late payment is damaging, the consequences escalate rapidly with subsequent or prolonged missed payments. Severity isn’t linear; it compounds over time, creating a cascade of negative effects.

- Severity Increases with Payment Timeline: Each stage of delinquency carries heavier penalties:

- 30 Days Late: The initial hit occurs, as described above. Your lender reports the delinquency, and your score takes the first major dive.

- 60 Days Late: A second consecutive missed payment is reported, further eroding your score. Lenders view this as a heightened risk indicator.

- 90 Days Late: This is a critical threshold. At this point, the risk of account closure skyrockets. Your creditor may decide to close the account entirely, severely limiting your available credit and significantly worsening your credit utilization ratio (another key scoring factor). The negative mark itself becomes more severe.

- 120+ Days Late: Once an account reaches 120 days past due, it’s often deemed uncollectible by the original creditor. This frequently leads to the account being charged off and potentially sent to collections. A charge-off is a major derogatory mark, indicating the creditor has given up on collecting the debt as agreed. If sold to a collection agency, a separate negative collection account is added to your report. Both the original charge-off and any collection account can remain on your credit report for up to seven years from the date of the first delinquency that led to the charge-off/collection.

Delinquency Timeline & Consequences:

| Days Past Due | Credit Bureau Reporting | Primary Consequences | Long-Term Impact |

|---|---|---|---|

| 1-29 Days | Typically not reported | Late fees charged by creditor | Minimal direct score impact |

| 30 Days | Reported as “30 days late” | Significant score drop (often 50-meaningful score movement); Lender risk alert triggered | Stays on report 7 years |

| 60 Days | Reported as “60 days late” | Further score decline; Increased lender concern; Possible credit limit reduction | Stays on report 7 years |

| 90 Days | Reported as “90 days late” | High risk of account closure; Severe score damage; Utilization ratio worsens | Stays on report 7 years |

| 120+ Days | Charged-off status reported; Potential collection account added | Account closed & charged off; Collection agency involvement; Catastrophic score impact | Remains 7 years from DOFD |

The journey from a single late payment to charge-off and collections illustrates how quickly manageable debt can spiral into a long-term credit burden. Addressing late payments promptly is vital to halt this domino effect. While the marks remain for years, their impact lessens over time, especially as you rebuild positive history. Strategies like goodwill letters for isolated lapses or professional credit repair assistance (available through resources like fixcreditscenter.com) can become essential tools for mitigating the damage and accelerating recovery.

Audit Your Credit Reports Like a Pro

The damage caused by late payments, as outlined previously, is heavily documented within your credit reports. These files, maintained by the three major credit bureaus (Experian, Equifax, and TransUnion), are the foundation your credit scores are built upon. Ensuring their accuracy isn’t just good practice; it’s a critical first step in repairing the damage from past delinquencies. Mistakes happen, and they could be unfairly dragging your score down even further.

Spotting Report Errors That Hurt You

Finding errors requires a meticulous, line-by-line review of each credit report. Don’t just glance – scrutinize. Focus especially on accounts where you had late payments, as reporting inaccuracies are common here. Look for:

- Payments Misreported as Late When Paid On Time: This is perhaps the most damaging error you can find. Check the payment history grid for every account meticulously. Verify that the months marked “30,” “60,” “90,” or “120” days late truly align with when you actually paid late. A payment processed a day late by your bank might have been reported as 30+ days late incorrectly. Gather your bank statements or payment confirmations as proof.

- Outdated Late Payments (>7 Years Still Showing): Federal law (the Fair Credit Reporting Act – FCRA) mandates that most negative information, including late payments, must be removed after seven years from the date of the first delinquency that led to the negative status (the Original Delinquency Date – DOFD). If a late payment from 2018 or earlier is still appearing on your 2026 report, it’s obsolete and must be disputed for removal.

- Incorrect Balances or Credit Limits: While less directly tied to payment history, errors here impact your credit utilization ratio, a key scoring factor. Ensure reported balances reflect what you actually owed at the time of reporting, and credit limits are accurate.

- Accounts That Aren’t Yours: Fraudulent accounts or accounts belonging to someone with a similar name (a “mixed file”) can appear, often with negative history attached.

- Duplicate Collections: Sometimes the same debt is listed multiple times, perhaps by the original creditor and a collection agency, or by multiple collection agencies, unfairly multiplying the negative impact.

Common Credit Report Errors & Their Impact:

| Error Type | Why It Hurts | What to Look For |

|---|---|---|

| Misreported Late Payment | Directly damages payment history (35% of FICO score) | Payment history grid showing “30/60/90+” late in months you paid on time |

| Obsolete Late Payment | Negative info illegally remains, suppressing score | Late payments with DOFD older than 7 years |

| Incorrect Account Status | Open accounts shown closed or vice versa, closed accounts shown charged-off | Account status flags (“Open”, “Closed”, “Charged Off”) not matching reality |

| Wrong Balance/Limit | Skews credit utilization ratio (30% of FICO score) | Reported balance much higher than actual; Credit limit lower than actual |

| Accounts Not Yours | Associates someone else’s bad history with your file | Accounts you never opened; Names/addresses you never used |

| Duplicate Collections | Same debt listed multiple times, exaggerating severity | Same creditor/debt amount listed under different collection agency names |

Dispute Tactics That Actually Work

Finding an error is only half the battle; you need to get it corrected or removed. The FCRA gives you the right to dispute inaccurate information. Here’s how to navigate the process effectively in 2026:

Step-by-Step Credit Bureau Dispute Process

- Document Collection is Key: Before you dispute, gather concrete proof. For a misreported late payment, this means copies of bank statements showing the payment cleared before the 30-day late reporting threshold, payment confirmation emails, or canceled checks. For obsolete information, calculate the DOFD from your records. Proof is your ammunition.

- Initiate the Dispute:

- Online Dispute Portals: All three major bureaus offer online dispute systems (Experian Dispute Center, Equifax Dispute, TransUnion Dispute). This is often the fastest method. You can typically select the specific item, choose the reason for dispute (“not mine,” “inaccurate date,” “obsolete”), and upload supporting documents directly. Keep screenshots of your submission.

- Certified Mail Options: For complex disputes, significant errors, or if you want a detailed paper trail, sending a dispute letter via certified mail with return receipt requested is still highly effective. Your letter must clearly identify each disputed item (account name, number, specific error), state the facts, explain why it’s wrong, include copies (never originals) of your proof, and request deletion or correction. The Consumer Financial Protection Bureau (CFPB) provides sample dispute letter templates.

- The Investigation Trigger: Once received, the credit bureau has 30 days (with some exceptions, like if you submit additional information during the investigation) to investigate your dispute. They forward your claim and evidence to the data furnisher (the lender or collection agency that reported the information).

- Furnisher’s Response: The furnisher must investigate your claim, review their records, and report the results back to the credit bureau. If they verify the information is accurate, it stays. If they find it’s inaccurate or cannot verify it within the timeframe, the bureau must remove or correct the item.

- Review Results: The bureau will notify you of the results of the investigation in writing and send you an updated copy of your credit report if changes were made. Review this carefully.

- If the Dispute is Rejected (But You’re Right): Don’t give up. You can:

- Re-dispute with New Evidence: If you have stronger proof, submit a new dispute.

- Dispute Directly with the Furnisher: Send your dispute letter and evidence directly to the lender or collection agency.

- Add a Statement of Dispute: You have the right to add a brief statement (100 words or less) to your credit file explaining your side, which future lenders will see.

- Seek Professional Help: For persistent, complex errors, or if the process feels overwhelming, reputable credit education resources, such as those accessible through fixcreditscenter.com, specialize in navigating disputes and leveraging consumer protection laws.

Successfully removing inaccurate negative items, especially wrongly reported late payments or obsolete delinquencies, can lead to a noticeable and sometimes substantial credit score increase. It eliminates unfair penalties. However, remember that accurately reported late payments will remain for seven years. The power of auditing lies in ensuring only the correct negatives impact your score. Consistent monitoring of your reports, at least annually (and more frequently when rebuilding), is the cornerstone of maintaining control. Leveraging tools like free annual reports or credit monitoring services, combined with knowing your dispute rights, empowers you to protect your score from errors as you work to rebuild positive history. Resources like fixcreditscenter.com can provide further guidance and support tailored to navigating these specific credit challenges in 2026.

Strategic Damage Control Playbook

While disputing errors tackles inaccurate late payments, accurately reported delinquencies require a different strategy: proactive engagement with your creditors. Moving beyond the credit bureaus and dealing directly with the source can yield surprising results, especially when combined with smart payment habits.

Negotiate With Creditors Directly

Don’t underestimate the power of asking. Creditors aren’t obligated to help, but many will consider adjusting your history, especially if you have a generally positive relationship and the lapse was uncharacteristic. This is particularly crucial for accurately reported late payments that disputes can’t remove.

Goodwill letter approach for isolated incidents

A goodwill letter is a formal request asking a creditor to remove a legitimately reported late payment as an act of courtesy. Success hinges on the nature of the lapse and your history:

- Ideal Candidates: This tactic works best for a single, recent (within the last 1-2 years) late payment on an otherwise spotless, long-standing account. An isolated mistake due to a temporary hardship (medical issue, job loss, simple oversight) is more likely to garner sympathy than a pattern of delinquency.

- Template Structure (Key Elements):

- Explanation (Brief & Sincere): Clearly state the account and the specific late payment month(s). Explain briefly and honestly why the late payment occurred. Avoid lengthy excuses; focus on taking responsibility (“I understand I missed the payment due on [Date] due to [Brief, genuine reason like ‘an unexpected medical bill’ or ‘a banking error on my part’]”).

- Highlight Positive Payment History: Emphasize your history as a reliable customer. Provide context: “Prior to this incident, I maintained a perfect payment history for [X] years/months on this account,” or “I have been a loyal customer since [Year].” Mention if you’ve always paid more than the minimum or kept a low balance.

- Express Regret & Current Status: State your regret for the lapse and assure them it doesn’t reflect your usual financial responsibility. Mention that the account is now current and in good standing.

- The Specific Request: Clearly and politely ask them to consider removing the late payment notation from your credit reports as a goodwill gesture. Use phrases like: “Would you please consider making a goodwill adjustment to remove this single late payment from my credit report?” or “I kindly request that you update the reporting to reflect my otherwise perfect payment history.”

- Professional Closing: Thank them for their time and consideration. Include your full name, account number, contact information, and signature.

Higher success with longstanding customer relationships: Your chances improve significantly if you have a deep history with the lender. Mentioning your tenure and overall positive standing reinforces that this was an anomaly, not a habit. Send the letter directly to the creditor’s executive office or customer relations department (find the address online) via certified mail for tracking.

Manage Expectations: Creditors have no legal obligation to comply. Many large institutions have strict policies against goodwill adjustments, especially automated systems. However, for smaller lenders or credit unions, or if you catch a sympathetic human reviewer, it can work. It costs little to try, especially for that one blemish on an otherwise clean record.

Payment Rehabilitation Techniques

Cleaning up past mistakes is vital, but stopping new late payments and strategically managing current debt is how you truly rebuild momentum. Focus on systems and priorities.

Catch-up strategies for current accounts

If you’re behind on payments right now, stopping the bleeding is paramount. Your immediate goals are: 1) Get all accounts current. 2) Ensure no more late payments occur. 3) Reduce high balances dragging down your score.

Automatic Payment Setup Promises Future On-Time Payments:

- The Ultimate Safeguard: This is the single most effective tool to prevent future late payments. Set up automatic minimum payments for every credit account through your bank’s bill pay or directly with each creditor. This acts as your safety net.

- 2026 Tools: Modern banking apps and creditor portals make this easier than ever. Set alerts a few days before payment is due to ensure funds are present. While autopay handles the minimum, you can always log in to make larger manual payments.

- Psychological Benefit: Removing the reliance on remembering due dates eliminates a major source of potential error and stress. Consistency is key for credit score recovery.

Balance Payoff Plans Targeting High-Credit Utilization First:

- Why Utilization Matters: Your credit utilization ratio (total balances / total credit limits) is a major FICO scoring factor (about 30%). High utilization (generally above 30%, lower is better) signals risk and hurts your score significantly, even if you pay on time. Late payments compound this damage.

- The Strategy:

- Prioritize High Utilization: While making minimums on all accounts, focus any extra funds on paying down the cards or loans with the highest utilization percentage first. Reducing a maxed-out card from 100% to 50% utilization gives a bigger score boost than reducing a card from 50% to 25%.

- Avalanche vs. Snowball (Utilization Focus): The purest utilization strategy is targeting the highest % first. However, if you need psychological wins, consider paying off the smallest balance first (snowball method) to free up cash flow quickly, then immediately redirect that payment amount to the account with the next highest utilization.

- Avoid Closing Accounts (Usually): Once paid off, keep old accounts open (even if you don’t use them much) unless they have high fees. Closing accounts reduces your total available credit, which can increase your overall utilization ratio and hurt your score. Use the card for a small purchase occasionally to keep it active.

- Seek Lower Rates: If you have decent credit despite the late payment (or after some cleanup), call creditors and ask for a lower interest rate (APR). A lower rate means more of your payment goes towards the principal, helping you pay down the balance faster. Balance transfer cards can be an option for high-interest debt, but tread carefully – they often require good credit and have fees, and a new late payment would be catastrophic.

Combining Forces: Imagine successfully getting an old late payment removed via goodwill and simultaneously reducing your credit card utilization from 80% to 30% through disciplined payoff. This one-two punch can trigger a significant score jump. The key is relentless focus on both correcting the past and mastering the present. Tools and personalized payoff strategies available through resources like fixcreditscenter.com can streamline this process in 2026, helping you prioritize effectively and track your progress towards a stronger score.

Rebuild Your Credit Foundation

Proactive creditor negotiation and rigorous payment habits stop the bleeding, but true credit score resurrection requires rebuilding positive history. Secured credit cards and strategic authorized user status are your most accessible tools for demonstrating renewed reliability to the bureaus in 2026.

Secured Credit Card Bootcamp

Secured cards function like training wheels for credit repair. You provide a cash security deposit (typically $200-$500), which usually sets your credit limit. This deposit minimizes risk for the issuer, making approval possible even with recent late payments. Used correctly, a secured card reports positive payment history monthly, directly counteracting past delinquencies.

How $200 deposits build $700+ scores:

- promised Positive Reporting: Unlike unsecured cards, secured card issuers readily approve applicants with poor or damaged credit. Every on-time payment you make is reported to all three major credit bureaus (Experian, Equifax, TransUnion), systematically building a new track record of reliability.

- Low-Risk Credit Utilization Practice: Your deposit-backed limit forces responsible spending. Aim to keep your balance below 30% of the limit (ideally below 10%) each month and pay the statement balance in full and on time. This demonstrates excellent credit management without accruing high-interest debt.

- Pathway to Unsecured Credit & Deposit Return: After 12-18 months of flawless use, many secured cards “graduate” to unsecured versions. Your security deposit is refunded, your limit may increase, and you retain the positive history built. This transition is a major milestone in score recovery.

Top 2026 Secured Card Options:

| Feature | Capital One Platinum Secured | Discover it® Secured |

|---|---|---|

| Min Deposit | $49, $99, or $200 | $200 |

| Reports To Bureaus | Yes (All 3) | Yes (All 3) |

| Credit Building Focus | High (49% eligibility factors for poor credit) | High + Rewards |

| Key Benefit | Potential for higher starting limit | Cashback Rewards (2% Gas/Restaurants, 1% Else) + Graduation Program |

| Best For | Lowest possible initial deposit | Earning rewards while rebuilding |

- Capital One Platinum Secured: Stands out for its potential lower deposit requirement ($49 or $99 for some applicants) and relatively higher reported eligibility factors (around 49%) for those with poor credit histories. It offers a straightforward path to building credit.

- Discover it® Secured: Uniquely offers cashback rewards (2% cash back at gas stations and restaurants on up to $1,000 in combined purchases each quarter, 1% on everything else) and a clear graduation program. Discover automatically reviews your account starting at 8 months for potential upgrade to an unsecured card and deposit return.

Action: Apply for one secured card. Treat it like gold – never miss a payment, keep utilization ultra-low, and pay in full monthly. This disciplined use is your fastest track to establishing a positive foundation.

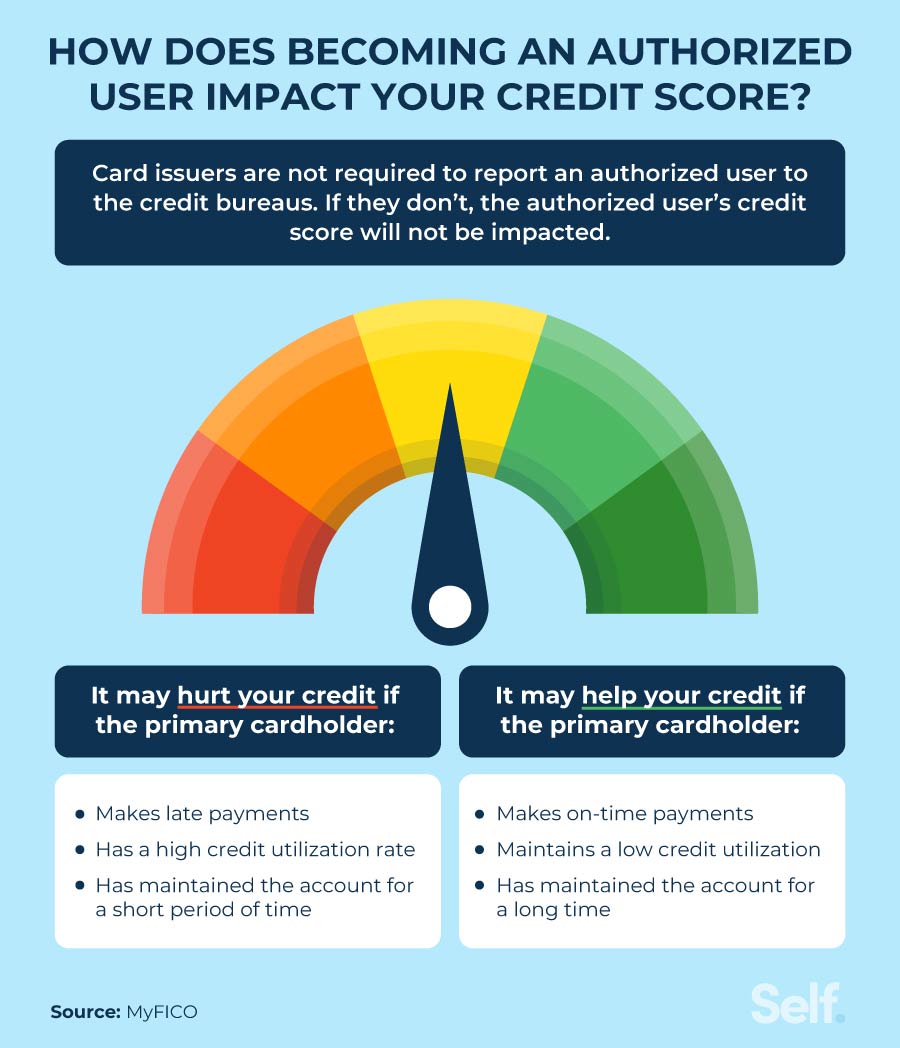

Become an Authorized User Strategically

Piggybacking on someone else’s excellent credit history can provide an instant boost. As an authorized user (AU), you’re added to another person’s existing credit card account. If managed correctly, the account’s entire positive history (including its age and payment record) can be added to your credit reports.

Piggybacking done right

This strategy is powerful but requires precision. A misstep can backfire or damage the primary user’s credit.

- Verify Issuer Reports to Credit Bureaus: Crucially, not all issuers report authorized user activity to all credit bureaus, and policies can change. Before being added:

- The primary cardholder must call their issuer and explicitly ask: “Do you report authorized user activity to all three major credit bureaus (Experian, Equifax, and TransUnion)?” Get confirmation in writing if possible.

- Confirm which bureaus they report to (it might not be all three). This step is non-negotiable in 2026. If the account isn’t reported to your credit files, you gain zero benefit.

- Ideal Candidate: Family Member with 5+ Year Perfect History: The primary account must be stellar:

- Long History: Ideally 5-10+ years old. This significantly boosts your “Average Age of Accounts.”

- Impeccable Payment Record: Absolutely no late payments, ever, on this account. Any negative mark (late payment, high balance) on the primary account will also land on your reports, harming your score.

- Low Utilization: The primary user consistently keeps the balance well below the credit limit (under 10-30% is ideal). High utilization on the AU account hurts your score too.

- High Trust & Communication: The primary user must be financially responsible, trustworthy, and willing to communicate openly about card use. You should agree upfront whether you’ll receive a card to use or if this is purely for credit reporting.

- Avoid Pitfalls:

- Never Use the Card Without Agreement: If you use the card, spending must be minimal, agreed upon, and paid back immediately to the primary user. Your spending impacts their utilization and debt.

- Primary User’s Responsibility: The primary user remains 100% legally liable for all charges. Your actions (or theirs) can damage both credit scores.

- Removal is Possible: If the situation sours or the primary account develops issues, you can request removal as an AU. The positive history may eventually drop off your reports, but any negative history reported while you were an AU might remain for up to 7 years.

Strategic Use: Becoming an AU on a pristine, ancient account can provide an immediate positive history injection, complementing your secured card efforts. This one-two punch – actively building with a secured card and passively benefiting from established good history – creates powerful momentum. Platforms like fixcreditscenter.com offer tools to track the impact of these strategies on your specific reports in 2026, helping you optimize your rebuild timeline.

Advanced Credit Repair Tactics

Rebuilding with secured cards and strategic authorized user status lays a crucial foundation, but tackling existing negative marks requires more specialized maneuvers. Let’s cut through the noise on two advanced tactics for 2026.

Pay-for-Delete: Myth vs Reality

The allure of “Pay-for-Delete” (PFD) is strong: pay a collection and have it completely erased from your credit reports. Unfortunately, the reality is far messier than the myth.

- The Core Myth: The idea that any collection account can be removed simply by paying it off in exchange for deletion.

- The 2026 Reality: Legitimate PFD agreements are rare, heavily contingent, and come with strict limitations:

- Only Third-Party Collectors Might Play Ball: Original creditors (like your old credit card company or loan provider) almost universally refuse PFD. They are bound by stringent reporting agreements with the credit bureaus. Your target, if any, is the third-party collection agency that bought or was assigned the debt.

- Written Agreement is Non-Negotiable: A verbal promise is worthless. Crucially, get the PFD agreement in writing before sending any payment. The letter must explicitly state the collection agency will request deletion of the specific tradeline from all three major credit bureaus upon receipt of your agreed payment. No written Promise? Walk away – paying might just update the status to “Paid Collection,” which still hurts your score (though less than an unpaid one).

- Success is Unpredictable: Even with a written agreement, there’s no absolute Promise the bureaus will comply with the collector’s deletion request. Agencies have less leverage than you think. Weigh the cost of payment against the uncertain outcome.

- Ethical & Reporting Gray Area: While not illegal per se, PFD skirts the spirit of accurate credit reporting. This inherent tension contributes to its scarcity.

When Negotiation Might Be Worth Attempting: Focus efforts on smaller, newer (less than 2 years old), third-party collections where you have clear written PFD terms. For older debts, paid collections, or debts with original creditors, PFD is almost certainly off the table. Dispute inaccuracies instead. Platforms like fixcreditscenter.com provide tailored dispute templates aligned with the latest 2026 FCRA guidelines.

Credit Counseling Deep Dive

Nonprofit credit counseling can be a lifeline, but not all agencies operate equally. Understanding the distinction between nonprofit and for-profit models is critical in 2026.

| Feature | Nonprofit (NFCC Member Agency) | For-Profit Credit Counseling |

|---|---|---|

| Primary Focus | Education & Debt Management Plans (DMPs) | Profit generation, often via high fees |

| Fees (DMP Setup/Monthly) | Typically $0-$75 setup / Avg. $40-$79 monthly | Often $50-$200+ setup / $50-$100+ monthly |

| FICO Impact Potential | Avg. +7 points in 6 months (via on-time DMP payments & reduced utilization) | Highly variable, often less effective |

| Counselor Certification | Mandatory NFCC certification & training | No universal standard |

| Transparency | Required fee disclosure & budget review | Fees often obscured or bundled |

| Creditor Relationships | Established agreements for lower interest rates | May lack formal creditor relationships |

Navigating the Nonprofit vs For-Profit Divide

Nonprofit Agencies (NFCC – National Foundation for Credit Counseling):

- Structure & Mission: Operate under 501(c)(3) status. Their primary goal is client financial health, funded partly by “fair share” contributions from creditors participating in DMPs (creditors agree to this because DMPs increase recovery rates).

- Fee Caps & Value: Setup fees are low or waived; monthly DMP fees are federally recommended to be capped at $79, with many reputable agencies charging $40 or less. A 2026 industry analysis shows NFCC agency clients enrolled in DMPs see an average FICO score increase of approximately 7 points within the first 6 months, primarily due to consistent on-time payments reported through the plan and reduced credit utilization as debts are paid down.

- Services: Comprehensive budget counseling, debtor education, housing counseling, and DMPs if appropriate. DMPs consolidate unsecured debt payments, often with reduced interest rates and waived fees negotiated with creditors.

- Verification: Always confirm an agency is a member of the NFCC (nfcc.org) – the industry’s gold standard for ethics and training.

For-Profit “Credit Counseling” Services:

- Structure & Motivation: These are businesses focused on generating profit for owners/shareholders. Fees are their primary revenue source.

- Fee Pitfalls: Often charge significantly higher setup and monthly fees than nonprofits. Fees may be buried in complex agreements or bundled with other services of dubious value. The $79 monthly cap doesn’t apply.

- Service Risks: May push expensive debt settlement programs (harmful to credit) instead of legitimate DMPs or counseling. Quality of counseling and creditor negotiation leverage is often inferior.

- Red Flags: High-pressure sales tactics, promises of promised results or drastic debt reduction, lack of NFCC affiliation.

Action: If struggling with multiple payments or high interest rates, consult a NFCC-member nonprofit agency. They provide a free initial budget review and assessment. A well-managed DMP can streamline payments, save on interest, and create a structured path that reports positively to bureaus. Track your DMP’s impact on utilization ratios and score trends using tools available at fixcreditscenter.com. Avoid for-profit debt settlement mills masquerading as “counseling.”

Bulletproof Payment System Setup

Advanced tactics like pay-for-delete negotiations and credit counseling address past mistakes, but preventing future late payments is non-negotiable for sustained credit recovery. A meticulously designed payment system acts as your financial airbag. Let’s engineer yours for 2026.

Payment Automation Master Plan

Manual payments are a relic. Automation is your frontline defense against forgetfulness, busy schedules, or simple oversight. But not all automation is created equal.

| Automation Method | How It Works | Key Benefit for 2026 Credit Repair | Critical Consideration |

|---|---|---|---|

| Creditor Autopay | Pay directly from your bank account via the lender’s system on your chosen date. | Prevents 98% of human-error lates. Reports consistently as “paid as agreed.” | Ensure sufficient funds 3 days prior. Set for minimum unless paying in full. |

| Bank Bill Pay | Your bank sends payments electronically or by check on your specified schedule. | Centralized control. Good for creditors without robust autopay. | Allow 5-7 business days for check payments. Verify receipt. |

| Calendar-Driven Transfer | Automate transfers to a dedicated “bills” account aligned with due dates. | Segregates bill money, reducing accidental spending. | Requires strict discipline to only use this account for payments. |

Why Stacking Matters: Align payment due dates with your paycheck deposits. Contact creditors to request due date changes – most allow 1-2 changes per year. Having major payments hit shortly after payday drastically reduces cash flow strain.

Fail-safe calendar strategies

Automation needs backup. Layer these calendar strategies:

- Bi-Weekly SMS/Email Alerts: Set reminders for 3 days before each autopay draft and 1 day before any non-automated payment is due. Tools like Google Calendar, Apple Reminders, or dedicated bill-tracking apps offer customizable alerts.

- Weekly “Money Date”: Block 15 minutes every week (e.g., Sunday evening) solely to:

- Verify upcoming autopay drafts.

- Confirm payments processed from the previous week.

- Check bank balances against expected bills.

- Post-Paycheck Reconciliation: Within 24 hours of every paycheck landing:

- Schedule any non-automated payments due before the next payday.

- Transfer funds to your dedicated bills account.

- Review your calendar alerts for the upcoming pay period.

Emergency Fund Protection

Automation crumbles without cash flow. An emergency fund isn’t just for major disasters; it’s your shield against minor financial shocks causing late payments. Think car repairs, medical copays, or temporary income dips.

How $500 buffers prevent future lates

A starter fund of $500 is your critical first line of defense in 2026. Here’s why:

- Covers Minimums: $500 typically covers the minimum payments on 2-4 major credit cards or loans for one month, buying crucial time during a cash crunch.

- Prevents Cascade Failure: One unexpected expense won’t derail your entire payment schedule, stopping a single late payment from triggering multiple lates.

- Reduces Reliance on Credit: Avoids using high-interest cards to cover emergencies, which increases utilization and debt burden.

Building Your Shield:

- Start Small, Start Now: Aim for $500 first. Automate transfers of even $20-$50 per paycheck into a dedicated account.

- Target 3-Month Minimums: Your next goal: save the equivalent of 3 months’ worth of minimum payments on all essential debts (credit cards, loans). Calculate this total and make it your bullseye.

- Park it Smart: Stash this fund in a high-yield savings account (HYSA) earning 4.5% APY or higher. As of 2026, several reputable online banks offer FDIC-insured HYSAs in this range. This keeps the money liquid but working for you, outpacing inflation slightly. Do not invest this buffer – accessibility is key.

Integrate & Monitor: Link your HYSA emergency fund to your primary checking for rapid transfers if needed. Crucially, replenish any withdrawals immediately. Track your emergency fund growth and its direct impact on your payment consistency and credit score trends using tools available at fixcreditscenter.com. This tangible progress fuels motivation and proves the system works.

Tracking Your Credit Comeback

Advanced payment systems and emergency buffers lay the groundwork, but true credit recovery demands vigilant tracking. Understanding how and when your actions translate into score gains transforms patience into strategy. Here’s your 2026 roadmap for monitoring progress and recognizing milestones.

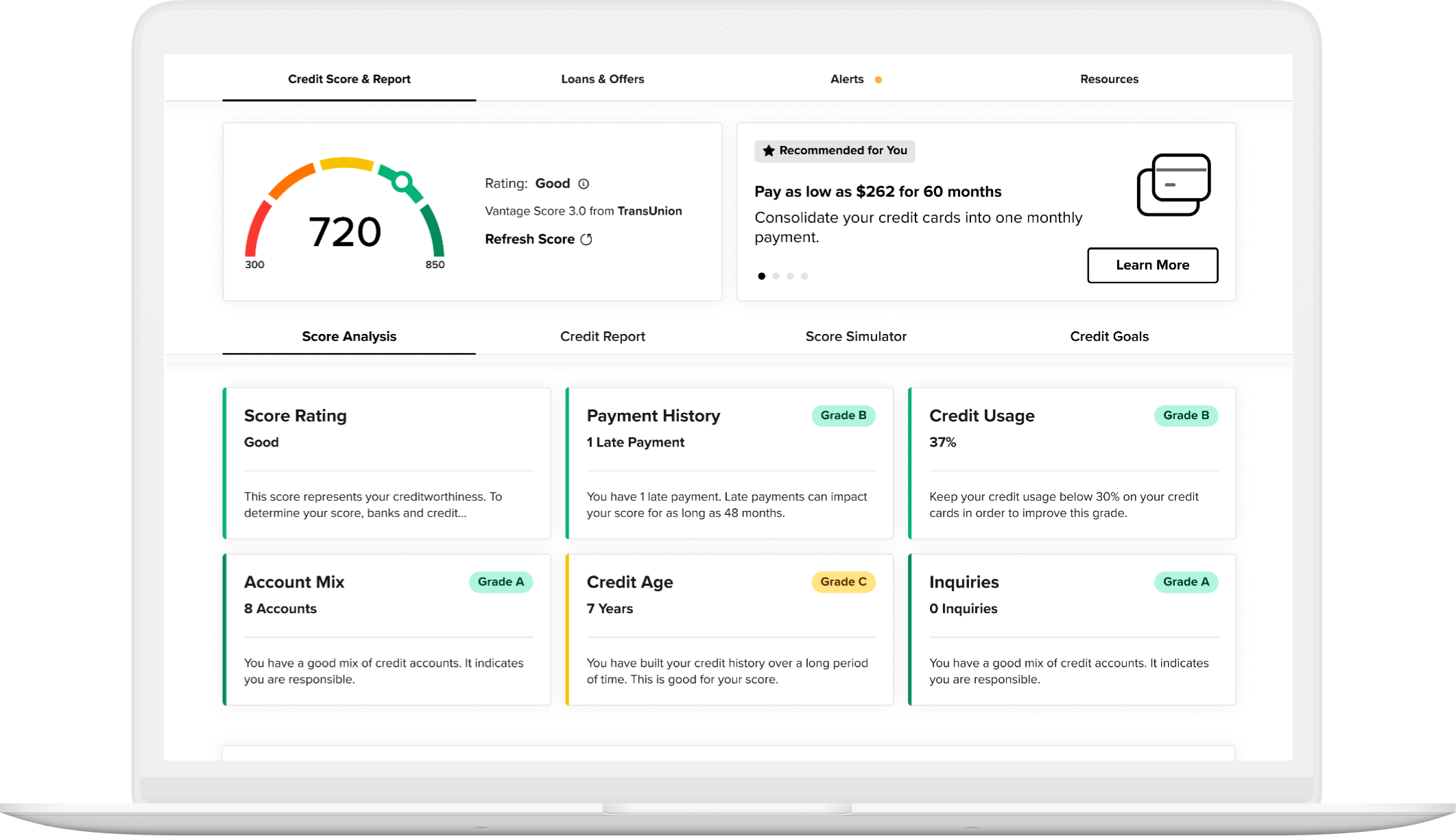

Credit Monitoring Showdown

Passively waiting for updates is a missed opportunity. Proactive monitoring in 2026 isn’t optional; it’s essential intelligence. But choosing the right tool matters. Free services offer accessibility, while paid tiers deliver the granular detail lenders actually use.

Free vs paid service features

| Feature | Free Services (e.g., Credit Karma) | Paid Services (e.g., Experian) | Why It Matters for Late Payment Recovery |

|---|---|---|---|

| Credit Score Model | VantageScore 3.0/4.0 | FICO Score 8 (Most widely used by lenders) | FICO scores reflect lender decisions accurately. |

| Score Update Frequency | Weekly | Monthly (or daily with premium) | Timely detection of score shifts post-payment. |

| Full Credit Report Access | Limited (summary views) | Unlimited access to full Experian report | Deep dive into why scores change. |

| Credit Report Alerts | Yes (changes reported) | Yes + Dark Web Scan & Identity Theft Insurance | Critical protection while rebuilding credit. |

| Score Simulators | Basic | Advanced (predicts impact of specific actions) | See how paying down a card affects your FICO. |

| Key Limitation | VantageScore ≠ FICO | Cost (typically $24.99-$39.99/month) | Free scores are useful trends, not lender grades. |

The 2026 Verdict: Start free (Credit Karma, Credit Sesame) for trend spotting and utilization alerts. Crucially, invest in tracking at least one FICO score monthly (Experian free trial or paid plan). Knowing your true FICO score and seeing the specific factors dragging it down (like “number of accounts with late payments”) is non-negotiable for targeted repair post-late payments. Services like Experian also provide precise dates when negative marks are scheduled to fall off your report – vital intel.

Milestone Celebration Guide

Rebuilding credit after late payments is a marathon, not a sprint. Recognizing key physiological turning points keeps motivation high and expectations realistic in 2026. Track these time-based inflection points:

Score improvement timeline

The 60-Day Utilization Win (Visible Shift):

- What Happens: The most immediate positive impact comes from drastically lowering your credit utilization ratio (below 30%, ideally below 10%). This is the fastest lever to pull. Reductions here can reflect in your score within 1-2 billing cycles.

- Celebrate This: Seeing a 20-50 point jump solely from paying down balances reinforces that current behavior matters intensely. Check your score after your new, lower balances report to creditors. This is your first tangible proof of progress. Action: Maintain this low utilization religiously.

The 6-Month On-Time Streak (Foundation Solidifies):

- What Happens: While late payments remain on your report, demonstrating 6 consecutive months of perfect, on-time payments signals strong recovery behavior to scoring models. This consistency starts to outweigh the recent negatives. Expect gradual, steady increases during this period.

- Celebrate This: Hitting the half-year mark without a single late payment is a major psychological and scoring hurdle cleared. Your score recovery gains momentum. Action: Double-check your automated payment system and emergency fund – they’re working! Tools at fixcreditscenter.com can visualize this positive payment trend.

The 2-Year Delinquency Dilution (Major Impact Halves):

- What Happens: The sting of a late payment lessens significantly over time. While a late payment stays on your report for 7 years, its negative impact on your FICO score drops substantially around the 2-year mark. It hasn’t vanished, but newer positive history carries more weight.

- Celebrate This: This is where disciplined recovery starts yielding major score returns. A late payment from 25 months ago hurts far less than one from 6 months ago. Qualifying for better loan terms becomes realistic. Action: Keep all accounts current and avoid new negatives. Monitor your report – ensure old lates are accurately dated and due to fall off on schedule.

Tracking these milestones isn’t just feel-good; it’s strategic validation. Seeing your FICO score climb as predicted confirms your system works. For precise tracking, personalized projections, and tools to manage every phase of your credit repair journey, leverage the resources available at https://fixcreditscenter.com. Their dashboards align perfectly with these key recovery timelines.

Key Takeaways for Credit Recovery

Late payments create long-lasting credit damage, but strategic action can accelerate your score’s recovery. Focus on these practical methods:

- Dispute inaccuracies – Remove wrongly reported late payments via credit bureau disputes

- Negotiate with creditors – Goodwill letters may address isolated late payments

- Rebuild positive history – Secured cards and authorized user status demonstrate new reliability

- Automate payments – Prevent future late payments with foolproof systems

Your credit score recovery starts today. For personalized tools and step-by-step guidance, visit fixcreditscenter.com now. Share your success story in the comments below!

Disclaimer

This article is for educational purposes only and does not constitute legal, financial, or credit repair advice. FixCreditsCenter.com does not promise credit score increases, credit approval, or removal of accurate negative information. Results vary based on individual credit history.