7 practical Ways to Fix Credit with Collections Fast

Did you know a single collection account can slash meaningful score movement off your credit score? Learn how collections work, their 7-year timeline, and actionable steps to minimize damage and rebuild your credit in 2026.

【Understanding Collections on Your Credit】

How Collections Damage Your Credit Score

Collections accounts are among the most damaging items on your credit report, primarily because they directly impact your payment history—the largest component of your FICO® Score, accounting for 35%. When a debt goes to collections, it signals to lenders that you’ve failed to repay an obligation, which can trigger immediate and severe score drops.

Payment history impact (35% of FICO® Score)

- Recent collections cause significant drops: For individuals with good credit scores (e.g., above 700), a new collection account can slash your score by up to large score jump or more. This is because FICO models prioritize recent negative events, and a collection entry acts as a major red flag. For instance, if a collection appears in 2026, it could push a 750 score down to the mid-600s over time, making it harder to qualify for loans or credit cards.

- Unpaid vs. paid status matters in older scoring models: In traditional systems like FICO 8, even if you pay off a collection, the account remains on your report and continues to hurt your score, as it still reflects past delinquency. However, newer models like FICO 9 treat paid collections more leniently, reducing their impact. This inconsistency highlights why addressing collections promptly is crucial; unpaid accounts drag down your score longer, while paid ones may offer some relief depending on the scoring version used by lenders.

Timeline for Collection Accounts

The duration a collection stays on your credit report is governed by the Fair Credit Reporting Act (FCRA), which sets a strict 7-year limit from the original delinquency date. This timeline starts when you first missed a payment on the original debt, not when the collection agency acquired it.

7-year reporting rule from first delinquency

- Example: May delinquency = May removal 7 years later: If your initial delinquency occurred in May 2026 (e.g., a missed credit card payment), the collection account must be removed from your credit reports by May 2032. This automatic deletion helps your score recover gradually as the item ages, but it remains visible to creditors during that period.

- Resold debts share original delinquency date: Even if a debt is sold multiple times to different collection agencies, the removal date is always based on the first delinquency. For example, a debt defaulted in 2026 and resold in 2027 would still fall off reports in 2032. This rule prevents agencies from restarting the clock, ensuring fairness. To accelerate credit repair, consider disputing inaccuracies or negotiating settlements. For expert guidance on navigating this process, services like fixcreditscenter provide tailored solutions—visit https://fixcreditscenter.com to explore options for resolving collections and rebuilding your financial health.

【Validating Collection Accounts】

Accurate reporting is foundational when tackling collections. Errors are common—debts may be listed multiple times, show incorrect balances, or even belong to someone else. Proactive validation ensures you dispute only legitimate inaccuracies, maximizing repair efficiency.

Accurate reporting is foundational when tackling collections. Errors are common—debts may be listed multiple times, show incorrect balances, or even belong to someone else. Proactive validation ensures you dispute only legitimate inaccuracies, maximizing repair efficiency.

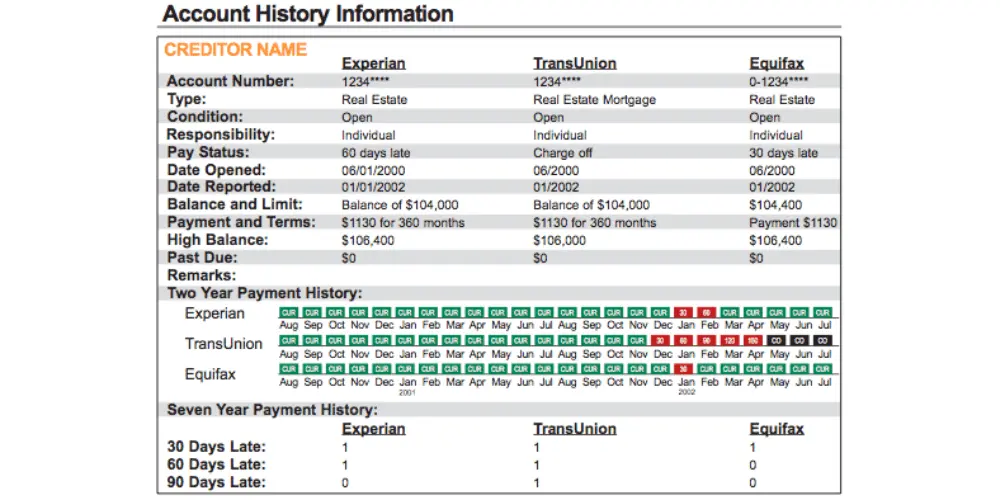

Review Your Credit Reports

Start by obtaining reports from all three major bureaus (Experian, Equifax, TransUnion). Discrepancies between them are red flags requiring action.

Obtain free reports from all 3 bureaus

- AnnualCreditReport.com: Weekly free access: Under federal law, you can access reports weekly at no cost until December 2026. This replaces the pre-2026 annual limit, enabling frequent monitoring—crucial for tracking collection disputes.

- Check for account amounts/statuses: Scrutinize each collection entry. Verify:

- Original creditor name and current collector

- Reported balance vs. actual debt

- Dates (first delinquency, collection placement)

- Status (“unpaid” vs. “paid in full”)

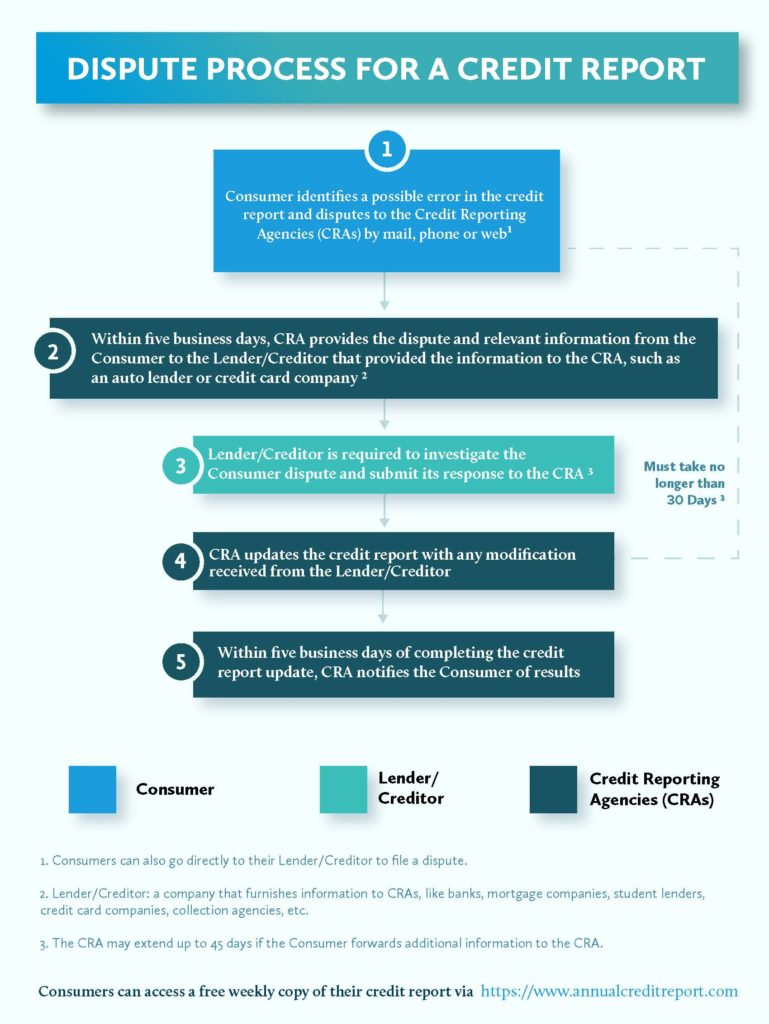

Dispute Inaccurate Information

If you spot errors (e.g., incorrect balances, duplicate entries, expired accounts), initiate disputes immediately. The FCRA mandates bureaus investigate within 30 days.

Credit bureau dispute process

Disputes can be filed online, by mail, or phone. Each bureau has dedicated channels:

| Bureau | Online Portal | Mail Address | Phone |

|---|---|---|---|

| Experian | experian.com/disputes | P.O. Box 4500, Allen, TX 75013 | 1-888-397-3742 |

| Equifax | equifax.com/dispute | P.O. Box 740256, Atlanta, GA 30374 | 1-866-349-5191 |

| TransUnion | transunion.com/dispute | P.O. Box 2000, Chester, PA 19016 | 1-800-916-8800 |

- 30-day investigation window per FCRA: Upon receiving your dispute, bureaus must contact the debt collector for verification. If the collector fails to respond or confirms inaccuracy, the item must be removed. Always keep copies of dispute letters and tracking numbers. For complex cases—like persistent reappearing debts or collector non-compliance—services like fixcreditscenter offer specialized dispute escalation and creditor negotiation to streamline resolution.

【Strategies for Collection Removal】

While disputing inaccuracies is essential, legitimate collection accounts require different tactics for removal. Negotiation and goodwill requests are key strategies.

While disputing inaccuracies is essential, legitimate collection accounts require different tactics for removal. Negotiation and goodwill requests are key strategies.

Negotiate Pay-for-Delete Agreements

A pay-for-delete agreement involves negotiating with the collector to remove the negative entry from your credit reports in exchange for payment. Success depends heavily on the collector’s policies and your negotiation skills.

Written agreement before payment

Never pay based on a verbal promise. Secure a written agreement explicitly stating the collection will be deleted upon receipt of payment. Insist on this before sending any funds.

- Sample clause to request: “In exchange for payment of $[Amount] as full settlement of account [Account Number], [Collection Agency Name] agrees to request deletion of this collection account from all credit bureaus to which it was reported within 30 days of cleared payment.”

- Success rate varies: Larger agencies and debt buyers are often less likely to agree than smaller, original creditors handling collections internally. Be prepared for refusal. If successful, retain the written agreement indefinitely.

Request Goodwill Deletion

If the collection is legitimate, paid, relatively minor, or aged, a goodwill deletion request asks the creditor or collector to remove it as an act of goodwill.

Effective for minor/old delinquencies

This approach works best under specific circumstances:

- The debt is paid in full: Creditors are more receptive once they’ve recovered the owed amount.

- The delinquency was isolated: A single late payment that led to collection is more likely to warrant goodwill than a pattern of non-payment.

- The account is older: Collections nearing the 7-year reporting limit (typically falling off your reports around 2026 if delinquency occurred in 2018) have less impact, making deletion easier to grant.

- You have a strong, longstanding positive history: Demonstrating consistently perfect payments on other accounts with the same creditor significantly boosts your case.

- You experienced a documented hardship: Briefly explain a genuine, temporary hardship (job loss, medical emergency) that caused the delinquency, emphasizing it was an exception, not the rule. Avoid excuses; focus on responsibility and recovery.

For complex negotiations, persistent issues, or if dealing with uncooperative collectors feels overwhelming, professional services like fixcreditscenter provide structured approaches and leverage to secure removal agreements.

【Handling Persistent Collections】

When pay-for-delete or goodwill requests fail, or if the debt remains unpaid, alternative strategies for managing persistent collections become necessary. Debt settlement and understanding the statute of limitations are critical components of this phase.

When pay-for-delete or goodwill requests fail, or if the debt remains unpaid, alternative strategies for managing persistent collections become necessary. Debt settlement and understanding the statute of limitations are critical components of this phase.

Debt Settlement Options

Settling the debt for less than the full amount owed can resolve the account and stop collection activity, though it impacts your credit differently than deletion.

Lump-sum settlement negotiations

Negotiating a lump-sum settlement involves offering a single, reduced payment to satisfy the debt. Success hinges on your ability to negotiate and the collector’s willingness to accept less.

- Typical reduction: 30%-60% of balance: Collectors often accept significantly less than the original balance, especially on older debts or accounts they’ve been unable to collect. Aim to start negotiations low (e.g., 30-40% of the balance) while being prepared to increase your offer if needed. Having the funds immediately available strengthens your bargaining position.

- Tax implications on forgiven debt over $600: The IRS generally considers forgiven debt exceeding $600 as taxable income. The collector may issue a Form 1099-C. Be prepared for potential tax liability on the forgiven amount. Consult a tax professional to understand your specific situation. Crucially, ensure any settlement agreement explicitly states the payment is “payment in full” and releases you from further liability. Get this agreement in writing before paying.

Statute of Limitations Considerations

The statute of limitations (SOL) dictates how long a creditor or collector can sue you to collect a debt through the courts. It is distinct from the credit reporting time limit (typically 7 years).

State-specific time limits (3-10 years)

The SOL varies significantly by state and debt type (written contract, oral agreement, promissory note, open-ended accounts like credit cards). Know your state’s specific laws.

- Legal collection window vs. credit reporting period: The SOL defines the timeframe for legal action (lawsuits). Once the SOL expires, the debt becomes “time-barred,” meaning a collector cannot win a lawsuit against you to force payment. However, the debt can still legally appear on your credit report for the full ~7-year reporting period from the date of first delinquency. Collectors might still attempt to collect time-barred debts, but you have legal defenses against a lawsuit.

- Partial payments restart the clock: Making any payment, or sometimes even acknowledging the debt as yours in writing, can restart the statute of limitations clock in most states. This gives the collector a fresh period to potentially sue you. Be extremely cautious about making payments or written agreements on very old debts without understanding your state’s SOL and the consequences. If a debt is near or past your state’s SOL, seeking legal advice before taking any action is prudent.

Navigating persistent collections, especially when negotiating settlements or dealing with statute of limitations complexities, can be challenging. For tailored strategies and expert negotiation support, consider consulting a reputable service like fixcreditscenter.

【Rebuilding Credit Post-Collections】

Successfully navigating collections is a significant step, but true credit repair requires actively rebuilding positive credit history. Utilizing specific tools and optimizing key credit factors are essential strategies to improve your credit score after resolving collection accounts.

Successfully navigating collections is a significant step, but true credit repair requires actively rebuilding positive credit history. Utilizing specific tools and optimizing key credit factors are essential strategies to improve your credit score after resolving collection accounts.

Credit-Building Tools

When traditional credit avenues are closed due to past issues, specialized tools offer a pathway to demonstrate renewed creditworthiness.

Secured credit cards

Secured cards are often the most accessible starting point. They require a refundable security deposit, which typically sets your credit limit.

- $200-$500 security deposit requirements: Most issuers require deposits starting around $200, with many options available up to $500. This deposit minimizes risk for the lender while giving you access to a revolving credit line that reports to the major credit bureaus.

- Graduation to unsecured cards in 12-18 months: Responsible use—keeping balances low and making all payments on time—can lead to your card “graduating” to an unsecured status. This usually happens within 12 to 18 months, resulting in the return of your deposit and potentially a higher credit limit without the security requirement.

Credit-builder loans

Unlike traditional loans, credit-builder loans are designed specifically to help establish or rebuild payment history. The structure is unique:

- Structure: Funds released after payment completion: You don’t receive the loan money upfront. Instead, the lender places the loan amount (e.g., $500) into a locked savings account. You make fixed monthly payments over the loan term (often 6-24 months). Only after successfully completing all payments do you receive the funds, plus any accrued interest.

- Typical amounts: $300-$1,000: These loans are generally small, commonly ranging from $300 to $1,000, making the monthly payments manageable. Each on-time payment is reported to the credit bureaus, building a positive payment history.

Optimizing Credit Factors

Beyond using specific tools, actively managing the core components of your credit score accelerates recovery.

Payment history rehabilitation

Your payment history is the single most influential factor in your credit score. Rebuilding it is paramount.

- Automatic payments prevent new delinquencies: Setting up automatic minimum payments for all credit accounts is the most reliable way to ensure no future late payments occur, preventing further damage to your score.

- 6+ months of on-time payments show improvement: While credit repair takes time, consistently making all payments on time for at least six months demonstrates tangible positive behavior to creditors and can start to yield noticeable score improvements. Consistency beyond this period further solidifies the positive trend.

Credit utilization management

Credit utilization (the percentage of your total available credit you’re using) is the second most significant scoring factor. Keeping it low is crucial.

- Ideal ratio: Below 30% (Under 10% best): While staying below 30% of your total available credit limit is a common guideline, aiming for under 10% utilization yields the best results for your credit score. This applies to individual card utilization and your overall combined utilization.

- Example: $3,000 limit = $900 max balance: If you have a credit card with a $3,000 limit, keeping the balance at or below $900 keeps you at the 30% threshold. To maximize scoring benefits, aim for a balance of $300 or less (10%) on that card whenever possible. Paying down balances before the statement closing date is key, as that’s when most card issuers report balances to the bureaus.

Rebuilding credit after collections requires patience and disciplined financial habits. For personalized guidance on navigating this process and leveraging the most effective tools for your specific situation, explore the resources available at fixcreditscenter.

【Monitoring Your Progress】

Successfully implementing credit-building tools and optimizing key factors requires diligent monitoring to understand your score’s response and ensure resolved collections are accurately reflected. Key differences in credit scoring models significantly impact how your resolved collections affect your score, making tracking essential.

Successfully implementing credit-building tools and optimizing key factors requires diligent monitoring to understand your score’s response and ensure resolved collections are accurately reflected. Key differences in credit scoring models significantly impact how your resolved collections affect your score, making tracking essential.

Credit Scoring Model Differences

Not all credit scores treat collection accounts the same way, especially after they are paid. Understanding these variations is crucial for interpreting your progress accurately.

FICO® Score vs. VantageScore® treatments

The two major scoring model families handle paid collections differently:

- FICO 8: Counts paid/unpaid collections: The most widely used version, FICO® Score 8, factors in both paid and unpaid collection accounts when calculating your score. Resolving a collection (paying it or settling it) may stop further damage from updates, but the account’s negative history still impacts your score under this model.

- FICO 9/VantageScore: Ignore paid collections: Newer models like FICO® Score 9 and VantageScore® 3.0 & 4.0 disregard collection accounts that have been paid in full or settled. Once resolved, these accounts no longer negatively impact your score under these models.

| Scoring Model | Treatment of Paid Collections | Treatment of Unpaid Collections |

|---|---|---|

| FICO® Score 8 | Counted as negative factor | Counted as negative factor |

| FICO® Score 9 | Generally ignored | Counted as negative factor |

| VantageScore® 3.0/4.0 | Generally ignored | Counted as negative factor |

Note: Lenders choose which scoring model to use, so you may encounter FICO 8 even as newer models gain adoption in 2026.

Tracking Credit Report Changes

Consistently monitoring your credit reports from all three bureaus (Equifax, Experian, TransUnion) is vital after disputing errors or resolving collections. This ensures corrections are made and helps identify any reappearing inaccuracies.

Dispute resolution timelines

Understanding the process and timelines helps manage expectations and identify necessary follow-up actions:

- 30-45 days for bureau investigations: After you submit a dispute regarding an error, including an inaccurately reported collection, the credit bureau legally has 30 days (45 days if based on your free annual report) to investigate your claim. They must forward your dispute to the data furnisher (the company reporting the information) and review the evidence provided.

- Continued reporting = CFPB complaint option: If the credit bureau investigation concludes but the disputed information (like an incorrect collection account) remains on your report without adequate correction or explanation, and you believe it’s still inaccurate, you have the right to escalate. Filing a complaint with the Consumer Financial Protection Bureau (CFPB) is a powerful next step to seek resolution.

Regularly reviewing your reports throughout 2026 allows you to confirm the removal of resolved collections and track the positive impact of your rebuilding efforts. For comprehensive tools and personalized strategies to monitor your credit health and navigate disputes effectively, visit fixcreditscenter.

Key Takeaways for Managing Credit Collections

Collections severely impact your payment history (35% of FICO® Scores), but strategic actions can mitigate damage. Always validate debts for accuracy, negotiate pay-for-delete agreements in writing, and understand your state’s statute of limitations. Rebuilding requires secured credit tools and consistent on-time payments.

Ready to take control of your credit? Visit https://fixcreditscenter.com today for expert guidance on resolving collections and boosting your score. Share your success story in the comments below!

Disclaimer

This article is for educational purposes only and does not constitute legal, financial, or credit repair advice. FixCreditsCenter.com does not promise credit score increases, credit approval, or removal of accurate negative information. Results vary based on individual credit history.